Nickel & Dimed

Since our last vehicle purchase in 2006, major technological and ecological strides have moved the industry forward. Getting squeezed? Still part of the process.

My wife and I bought a new car on Monday.

The last time we purchased a vehicle, our twins were three years old; this time, they are two weeks shy of 20. Can you sense how much we love the process?

Spending a big chunk of money goes with the territory, but what makes it especially stressful and unpleasant is the industry’s well-earned reputation for going to questionable lengths to extract every possible penny along the way.

Though there are exceptions to this tiresome norm, our search provided absolute clarity as to why so many people opt for CarMax when looking for a used car. While CarMax’s prices might be a bit steep, there is comfort in their no-haggle, what-you-see-on-the-price-tag-is-what-you-pay policy.

As much as I enjoy those commercials featuring the likes of basketball star Steph Curry, CarMax’s most powerful marketing agent is something else: the shady practices of traditional car dealerships.

But CarMax wasn’t an option for us. After weeks of narrowing our search, five weeks ago Bridgett and I identified a new car, a 2023 Hyundai Tucson hybrid, as our choice.

The model and color we sought wasn’t on any lot within a few hours’ drive, and the earliest delivery was estimated to be over three weeks away at a dealership 35 miles from home.

When we went to give a $1,000 deposit to “lock in” that vehicle, they initially tacked on $5,000 to the manufacturer’s suggest retail price (a $3,999 “market adjustment” and a $999 “protection pack” we neither needed nor cared for).

When demand exceeds supply, “market adjustments” occur, but we balked and walked. About 20 minutes later, after the salesman knew we weren’t bluffing, he called to report the “good news” that his manager had “given the green light.”

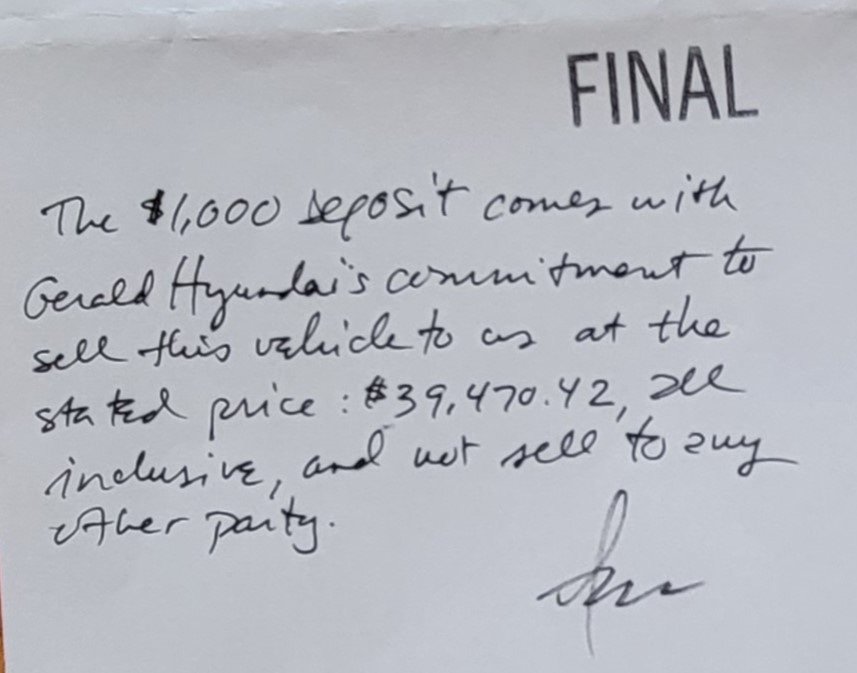

Still, our guard was up. When we made the deposit, it came only after I scrawled on the document:

“The $1,000 deposit comes with Gerald Hyundai’s commitment to sell this vehicle to us at the stated price: $39,470.42, all inclusive, and not sell to any other party.”

Three weeks became five weeks – that’s the supply chain disruption for you, no fault of the dealership – and we went to close the deal on Monday. First a test drive, then a tutorial from our perfectly genial salesman on all its cool bells and whistles.

It was all going so smoothly; I knew something was off.

Sure enough, when we went to fill out the final paperwork, the curveball came fluttering toward us. In effect, they said, “Whoops, we didn’t realize you lived in Cook County, so the sales tax is actually another $366.”

It was a ridiculous assertion. On our prior visit, they had made copies of our driver’s licenses. So, our Cook County residency was no mystery. Besides, we had that bottom-line price that had been mutually agreed to in June and stamped “FINAL” as you can see in the photo above.

Reason and an appeal to fairness and honesty didn’t move them. Next, I cited the “lifetime value of a customer” and my potential to provide a hearty endorsement about them to friends.

Didn’t matter.

Bumping the overall price up by 1% wasn’t going to kill this deal, not after the long, twisting journey we’d taken to this point just shy of the finish line. And they knew that, of course.

Nickel-and-dimed, right to the end.1

After agreeing to surrender the additional pound of flesh, I asked where their snacks were located.

“Are they in a vending machine?”

“No,” said the manager. “Help yourself.”

Testing the limits of my cargo pants pockets, I returned the nickel-and-dime favor. Yesterday morning, the Earl Grey tea was a nice complement to my breakfast.

I won’t be going back for more snacks — or another car, either.2

I recognize that there are far worse auto-purchase stories out there, including my own in 1992. That time, a salesman—a supposed “family friend”—duped me with a classic con-artist move. I expressed concern that my insurance costs would skyrocket when I went from a 1980 Toyota Supra worth maybe $1,000 to a Volkswagen GTI priced at about $13,000.

It was a Saturday afternoon, so I told him I’d check with my insurance agent on Monday. Only, this guy had a better idea: sitting right in front of me, he acted as if he was making a phone call to a “cousin” who was an insurance agent. As I looked on, this guy carried on what seemed to be an actual conversation, jotted down notes, then hung up the phone with wonderful news. My rates would be about the same as what I was already spending.

Wow! I was sold. (And really naive. And impatient. I couldn’t wait till Monday to confirm the figures with my agent?)

Turns out, my rates tripled – to $2,800 a year, or a shade over $6,000 in 2023 dollars. Such was the steep price of being an inexperienced 24-year-old car buyer. My biggest gift the following July, when I turned 25, was seeing that rate cut roughly in half.

So, no, I won’t be making an endorsement of Gerald Hyundai.

Though our own experiences have been positive, I could tell you plenty of horror stories. Good work on your addendum to the contract. Oddly enough, plenty of people seem to prefer the sense that they "got a deal" after the dealer comes down from whatever absurd number they started with. Remember Saturn, which was going to be sold with "no haggle" prices? Or when J.C. Penney tried to move to "fair and square" pricing? Here's a good piece on the topic. https://www.priceintelligently.com/blog/j-c-penny-s-pricing-strategy.

I highly recommend the Costco service to guarantee great value and cooperation in buying cars. No negotiating, no drama, and high satisfaction. Even for Honda and Hyundai. We saved over $2,500, and no frustration buying two different cars over 5 years.